1

Permanent Change of Station

Completing a Permanent Change of Station (PCS) often means adjusting to changes and starting new routines. This is especially true for your finances and cash flow.

Maria, an Army spouse, explains why she swears by having “healthy” PCS and emergency funds.

While the government provides relocation allowances to help cover the costs of a PCS, those allowances may not be enough to cover all of the expenses you will incur, or fully restore your financial situation to how it looks today.

Also, depending on where you move, the cost of living could be very different than what you’re used to now.

So, to keep your financial house in order, keep these tips in mind and tackle your next PCS like a pro.

Tips to Get Started

- Anticipate the PCS expenses you might incur before your move, during your move, and after you arrive at your new duty station.

- Use these two worksheets as you go through this section to help you estimate your costs for the move.

- Try to account for changes in both your family income and expenses from your previous duty station to the current one.

- Check if there are obligations you need to clear before leaving your current duty station.

- Do you have enough money available to pay for expenses until they’re reimbursed?

- What will your cash flow look like if you need to change jobs or your spouse's pay changes?

- Consider speaking with an accredited financial counselor at your installation’s family support center. He or she may offer spouse employment information, workshops and other resources to help family members locate jobs, update resumes, and even learn interview techniques. To locate a Personal Financial Manager, visit https://installations.militaryonesource.mil/

Kellie offers some financial tips to help you survive and thrive during your next PCS.

Financial Planning Considerations

A PCS move can be expensive! Here are some expenses that you could experience before your move.

- Cleaning, maintenance, and disassembling major appliances or backyard playscapes before you move can cost you more than you expected, so be sure to plan ahead.

- It’s probably not a big surprise that breaking a lease can cause you to lose your security deposit, but under the Servicemembers Civil Relief Act (SCRA), your PCS orders might qualify you to break your lease without losing your deposit. Consult your base legal office if you need additional help.

- Remember, you’re responsible for paying shipping expenses for items that exceed DoD weight limits. So, now might be a good time to lighten the load by having a yard sale! This might also help you avoid or reduce the costs of long-term storage for the stuff you plan to leave behind.

- It might make sense to purchase additional insurance on your household goods to cover potential losses beyond what the DoD will reimburse. Check with your renters or homeowners insurance provider to make sure you’re adequately covered.

- The cost of house hunting is your responsibility. The good news is, your spouse can take permissive temporary duty (TDY) to do it! The bad news is the DoD doesn’t pay for travel or lodging expenses, so just like all the potential housing expenses we’ve covered today, you should budget accordingly.

While these five things certainly don’t cover all of the expenses you might incur before your move, making sure you at least address them, should be a big help.

Now that we’ve talked about potential housing-related expenses you might incur before a PCS, let’s “shift gears” and talk about some vehicle-related items.

A lot of this, will depend on where you’re moving to and how you plan to get your vehicles there.

Let’s first explore four vehicle-related items that will apply to all PCS moves. Then, let’s look at a handful of points specific to OCONUS moves, which are moves outside of the continental United States.

- Insurance

Rates can vary from one location to the next. So, be sure to get informed and adjust your budget accordingly. Of course, you will also want to take this opportunity to notify your insurance provider that you’re moving so that you can get your policies updated. - Maintenance

Whether your PCS is stateside or overseas, now is probably a good time to get your vehicle ready for a safe trip or make sure it’s in good shape for when it gets to you. This could include things like getting new tires or brakes and getting an oil change. So, depending on the condition of your vehicle, you may need to set aside some money for this. - Vehicle Stays Behind

What if you’re not planning to take your vehicle, but instead plan to sell it or put it in storage? In this case, be sure to allocate money for transportation costs to get to your new location and, to get around once you’re there. - Leases

If you currently lease your vehicle, you may be able to break the lease under the Servicemembers Civil Relief Act. If this applies to you, check with your base legal office for more help.

Now let’s look at some additional considerations if your move is outside the continental United States.

- Number of Vehicles

Think about how many vehicles you plan to take. If you’re moving more than one vehicle, YOU will likely be paying for the extras. The government only pays for the shipment of one vehicle to overseas assignments, and usually only pays what it would cost to drive one vehicle from station to station in the continental United States. There may be exceptions, so check first with your command and your Travel Management Office. - Parts

Consider purchasing extra maintenance-related parts before you leave, since it may be hard to find them overseas, they could cost more, or there could be added expenses if you need them shipped. - Storage

If you plan to store your car instead of moving it, the government will pay storage fees up front. There may be exceptions to this, so confirm with your Travel Management Office first. Keep in mind that stored vehicles must remain in storage for the duration of the authorization orders. - Leased/Financed Vehicle

If you have a leased or financed vehicle, you may not be allowed to move your car overseas. Check with your leasing or financing company to learn what is permissible in your situation.

Now, let’s talk about some expenses you might have to deal with. These could include things like dinners out, and goodbye parties with friends. Or, if you’re moving overseas, there are several additional items to consider.

We’re talking about things like medical screening for dependents, immunizations, prescription refills, wisdom teeth extractions or braces.

Remember additional expenses you might incur for your pets, like immunizations, transportation costs, and quarantine fees.

It’s a good idea to prepare for the costs associated with passports and visas when transferring overseas. These vary based on whether the passport is new or being renewed. Even though these costs may be reimbursed with command approval. It’s still something to be prepared for.

Also, be aware that passport applications for children under 16 require the presence of both parents, even if they are estranged.

For more information on passport fees visit the State Department website at: www.travel.state.gov/passports.

That’s it for the major expenses before you PCS.

Although there are many different costs associated with a PCS, it’s smart to try to calculate reliable estimates ahead of time to avoid surprises.

So, you’re all packed up and ready to PCS! Now, let’s set some expectations about what it might cost to get you there.

Tips to Get Started

Financial Planning Considerations

Let’s use a case study to determine the cost of a PCS. To cover that, meet the Murray family.

Melissa Murray, wife of SGT Murray, and their beautiful family of three are moving from Ft. Stewart, Georgia to Ft. Drum, New York. The distance is about 1,000 miles. There are four main expense categories to consider here: driving, lodging, food and miscellaneous expenses, and recreation. Keep in mind, this is just a baseline for planning the cost of the trip. It has nothing to do with how much you will receive in reimbursements or entitlements.

First are driving costs. Allow an average of $25 per 100 miles of driving for gas and maintenance.

For the Murrays, this means they should plan for about $250 in driving expenses.

Next is lodging. The government authorizes 350 miles of travel per day. Use this to figure out how many nights you will be on the road. Then, plan for an average of about $120 per night for a hotel. If you have a larger family or pets, factor in a little more. The Murrays don’t have pets, so they’ll plan for $120 per night. For two nights (and three days) on the road, that will be about $240 for lodging.

The third expense category is food and miscellaneous expenses. Here, take the number of people traveling times the number of days, then multiply that by $50. For the Murrays, the math works like this:

3 people X 3 days X $50 = equals about $450 for food and miscellaneous expenses

These estimates may be different from the reimbursements or entitlements you would receive.

Visit your finance office or Transportation Management Office (TMO) for information about your specific situation.

This is our final PCS expense category. Yes, you can actually have some fun during this process. Instead of driving door-to-door, consider visiting friends and family along the way or do some sightseeing along the drive.

While some expenses may not be reimbursed, such as mileage, if you have the ability to sightsee, it might make the transition more enjoyable for the family.

Again, remember to keep all of your receipts!

So far, we’ve covered expenses and considerations before and during your PCS. Now let’s explore what to expect when you arrive.

Tips to Get Started

- Remember to make use of the resources on your installation to help you settle in more easily and save money.

- If you’re waiting on household goods, visit your installation’s lending closet. There’s no need to buy a new coffee maker. Borrow one!

- Visit your installation’s thrift store for great finds to help make your house a home or get creative with the furnishings you already own.

Are you thinking about purchasing a home during your next PCS move or preparing for a change in income because of your relocation? Watch Kellie’s video about being on the move with the military.

Financial Planning Considerations

In this section, we will break down key expenses for housing, transportation and other miscellaneous items.

Arriving at your new duty station often begins with you in temporary quarters, dining out and waiting on your household goods to arrive.

To save some cash, find a place with a small kitchen to avoid eating out.

If you don’t have a washer and dryer, expect to pay at least $3 to $6 per load of laundry at a laundromat.

The expenses change when you move into your new home.

Here, you may need to make security deposits, plan for extra trips to the exchange, and insure your home!

Let’s talk about security deposits. They’re pretty common when you rent a home, turn on utilities, or even connect to the internet. Sometimes they’re unavoidable, so plan ahead and set aside some extra cash to cover them.

If you’re counting on a refund from a previous security deposit, be patient. It could take 30 to 60 days to receive it.

When you move into a new home, utility companies may require you to pay a deposit to begin service. However, many companies will waive fees for service members or accept a letter of reference from your previous company to reduce fees, so be sure to ask.

It is inevitable. Once you arrive at your new home, you will probably realize you need some new stuff.

Expect to make extra trips to the exchange to restock things that didn’t move with you. Just make sure these purchases work within your budget and don’t put you into debt.

Don’t forget to insure your new home. Whether you are living in installation housing, renting a home, or you have purchased a home, contact your insurance provider to review and update your renters or homeowners policy as soon you move in. For more information, visit Renters Insurance and Homeowners Insurance.

After your move, look into registration requirements for your vehicles. You may be required to register in the state you move to.

Even if you’re allowed to keep your vehicle registered in a previous state, there may be new inspection requirements.

Also, be sure to update your auto insurance and adjust your budget if there is a new premium.

Review the policy details with your agent, as each state can vary on requirements. For more information, visit Auto Insurance.

- Cell phone plans: The Servicemembers Civil Relief Act may allow you to terminate your cell phone plan based on your PCS orders.

- Clothing: Perhaps you’ve moved to a new climate and need to update your wardrobe. Be smart, shop sales, and don’t forget the exchange.

- Your children: If you have kids, prepare for extra expenses when enrolling them in child care or school. Remember to budget for tuition, school uniforms, and other related costs.

2

Best Money Practices

Here are 10 financial tips to help make your PCS move go more smoothly.

Believe it or not, even though you’ll likely be moving to another state, that doesn’t mean you have to claim that state as your state of legal residence or domicile. This is true for both the service member, and his or her spouse. It’s important to give this issue some serious thought because your domicile can impact issues like state income taxes, personal property taxes, car registration, voter registration and others. Visit MilitaryOneSource.mil and search for "Military Spouses Residency Relief Act" to learn more.

Let’s face it, child care is a big expense, and often a necessary part of military family life, and the PCS process. The availability, cost, and location of child care can vary from one duty station to another. If you have children, it’s smart to begin researching your options and planning for changes to your budget as far in advance as you can. Be sure to check with your service’s family center to learn about programs that might help reduce some of the stress of moving.

Having cash on hand to cover added expenses will go a long way toward a successful move. You’re much better off drawing down savings than turning to high-interest credit cards to pay for things that come up.

Have a yard sale or do it online. The fact is, moving is a good time to purge non-essentials. A solid rule is to consider selling items you haven’t used in a year. This provides a double benefit — you make extra money and you lower your weight for shipping household goods.

Be sure to inform creditors, banks, brokerage firms, insurance companies, etc. before your move to avoid any missed communication or bills. You’ll also want to visit your local post office just before leaving to forward your mail.

As you plan your travel, try to use temporary lodging on military installations whenever possible to help reduce expenses. If that’s not an option, always ask for a military discount when booking civilian lodging.

If you don’t already do this, consider establishing electronic payments, transfers or allotments to pay your bills. This will help prevent missed payments while you’re in transit. Just be mindful of how you time them within the month so your cash flow covers these transfers and doesn’t leave you short.

Timing is important here, too. Don’t close current bank accounts until your new accounts are open and any automatic transfer for payment activity is reestablished. Consider banking at a financial institution that will serve you in various locations. That way, you can skip this step for your next PCS.

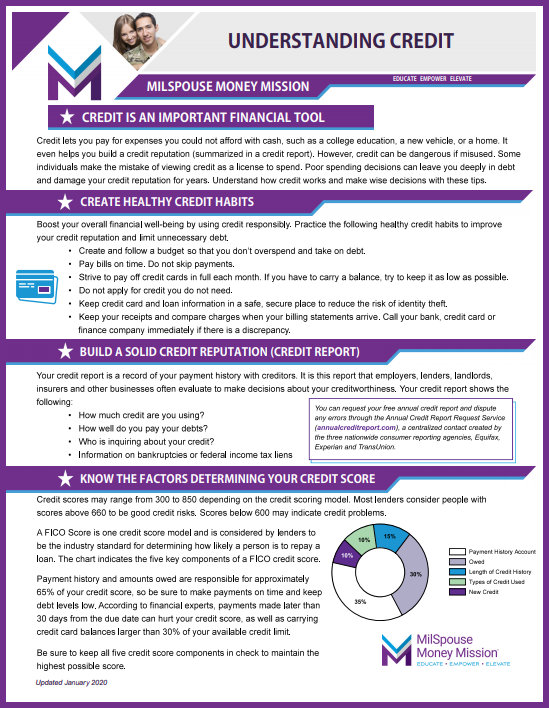

Whether you plan to rent or buy, your new landlord or lender will want to review your credit report, so it’s a good idea to check your report and resolve any errors before your move. Visit Understand Credit for more information about credit reports and credit scores, and how they can affect your financial life.

On the same note, it may be helpful to get a letter of reference from each of your utility companies before you leave, to show on-time payments and good records. Review this short handout for more information about credit reports and credit scores, and how they can affect your financial life.

Get preapproved before you begin shopping if you plan on buying a home or car at you next duty station. This can help you avoid emotional purchases, where you might take on more debt than you can realistically handle. Do the same if you need to buy another car.

You might even want to consider taking a class on home buying at your installation’s family center if you’re going to remain in that location after your spouse leaves the service.

3

Resources

Become familiar with the resources to make your next move, your best move.

https://www.militaryonesource.mil

This is a great site for information on the logistics of your PCS with links to service providers. Here, you can review your options, limitations and responsibilities with your upcoming PCS.

In addition to all the other great services they offer, you can find PCS related information by browsing, Plan My Move. Here you can enter your start and end destination and create a custom checklist to help you plan and carry out your move smoothly.

As we touched on earlier in this training, you can expect your service member to receive a number of travel pays and allowances as part of your PCS orders.

Typical examples include mileage reimbursement, per diem to cover hotels and meals, and a dislocation allowance. Depending on where you’re moving, your family might also receive an Overseas Housing Allowance, a Cost of Living Adjustment, a Move-In Housing Allowance, or a Temporary Lodging Allowance.

Your installation finance office or Travel Management Office can help you learn what’s applicable to your move.

Did you know that your service member can take an advance on his pay and eligible allowances like BAH prior to a PCS move?

While this could be helpful, remember any advance typically must be repaid over the following 12 months, so it may not be your best option. Here’s a BAH Calculator to help you make the best decision.

Remember, every family’s situation is different. Your needs, goals, and wishes are unique. What works for one family may not be right for you. Evaluate where you are and where you want to go. These tips and resources can help you get there.

Recent Blogs

March Money Moves: Navigating Tax Season While Preparing for Summer Fun

As we welcome the arrival of spring and the promise of warmer weather, it’s easy to get caught up in thoughts of summer plans and family vacations. But with tax season in full swing, it’s important to balance excitement for the upcoming months with a push to wrap up tax season. While those topics couldn’t…

Read More

Communicating with Your Partner About Finances: A February Focus on Financial Wellness

Talking Money with Your Partner As we celebrate loving relationships this month, it’s important to remember that not all conversations come up roses between couples. Sometimes discussing finances can be tricky and stir up negative emotions. Open communication about money is vital for building trust and nurturing a healthy relationship. Whether you’re a new couple…

Read More

Build Financial Wellness from the Ground Up in 2025

There’s something magical about the ball dropping at midnight and turning the page to a new year. For an instant, it feels like you’ve got a clean slate, and anything is possible. In some ways that’s true, but as the calendar page turns, your responsibilities, bills and financial challenges remain. Many people make resolutions to…

Read More

5 Financial Resolutions to Start the New Year Off Right

You don’t need to wait until January to take a fresh look at your finances. Get a jump on the new year with these five resolutions — they can really pay off over the next 12 months. 1. Set/update your budget Setting a budget is the first step in a military family’s financial planning. And…

Read More

5 Financial Power Moves for MilSpouses

During National Veterans and Military Families Month in November, we salute the strength of our families as they support the mission of our community. MilSpouses, especially, display determination as they face the challenges of military life. We see you navigate frequent moves, deployments and often raising children as a solo parent. We understand your motivation…

Read More

The Year In Review: Bring Your Financial Picture into Focus

It can be fun and even eye-opening to watch those year-end montages reminiscing about the year. If you ever have that moment when you say to yourself, “Wait, that was this year?”, you could also imagine how easy it could be to lose track of the goals and financial plans you set in motion when…

Read More

Now’s the Time to Think About Life Insurance

Hey, MilSpouses, it’s Life Insurance Awareness Month! Okay, so maybe that doesn’t make you want to break out the cake and ice cream, but life insurance is an important part of your financial plan. It can help take care of your family, giving them financial security if something happens to you or your service member.…

Read More

Budget and Insurance: What to Do After You PCS

After months of planning and hard work, you’ve landed safely at your next duty station. Congratulations! As you kick off this next chapter in your MilLife, it’s a good time to check in on your finances. Let’s look at two key items that are likely to change after a PCS: your budget and your insurance.…

Read More