1

Getting Started

The time leading up to a deployment is challenging, both logistically and emotionally. There are many details that need to be taken care of in a short period of time. Here you will find a checklist to help get your financial life in order prior to a deployment. Attention to these items ahead of time can mean big savings and help you achieve your financial goals moving forward.

But first, let's hear some deployment tips from Jeremy:

The first step is to know what special pay and entitlements your Service member may receive during deployment. To learn what some of those may be, visit the Defense Finance and Accounting Service website, or DFAS.

Then, factor any extra pay into your budget. Know what you will have coming in and going out. Both income and expenses can change during a deployment so it can be a great time to pay off debt, build your emergency fund, and put extra savings away for retirement. Set achievable goals and build a plan that works for you. Revisit your plan often and adjust as needed.

Listen to how Erica took advantage of deployment pay:

Online banking is a great way to keep track of your obligations. Ensure you have login credentials for all accounts and know payment schedule details like amounts and due dates.

You may have increased income during a deployment, so now would be a good time to check in on your emergency fund. Is it fully funded with three to six months of living expenses? We have all experienced unexpected expenses like home or car repairs that can bust your budget. And we all know deployments are when Murphy's Law tends to hit and stuff happens.

Use your emergency fund for these events and avoid using a credit card and paying interest or borrowing the money from someone. Think of this fund like a cushion that helps protect your family when life throws you financial curve balls.

Review your insurance coverage. Our Money Ready 201: Insure your Family covers the different types of insurance you should have and helps you determine how much is needed.

- Life Insurance — It is not an easy topic to discuss, but it provides priceless peace of mind. Everyone’s needs are different, so think L-I-F-E when considering how much life insurance you need:

L – Liabilities

I – Income to be provided

F – Final expenses

E – Education/other goals

- Add these values, subtract any assets, and your life insurance coverage should be greater than the calculation to ensure your needs are covered.

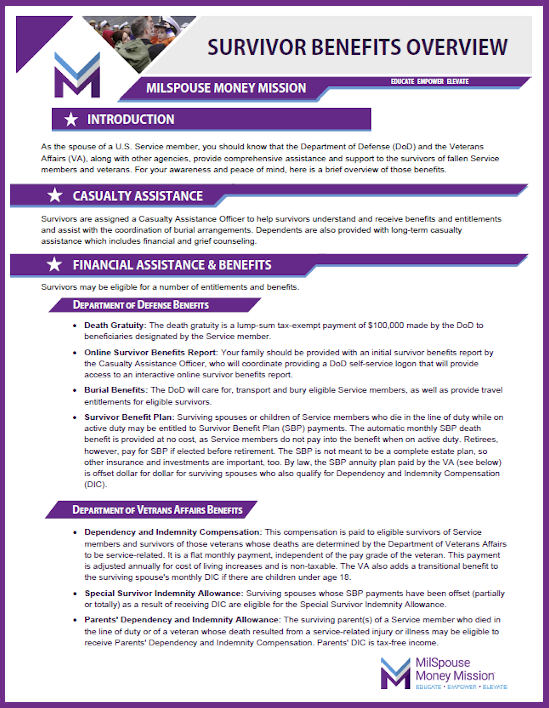

- Every Service member is provided $400,000 of term coverage under Servicemembers Group Life Insurance (SGLI) unless they decline or elect a lower amount. There is an additional $100,000 death gratuity for those killed in the line of duty. Additionally, there may be further benefits under the Survivor Benefit Plan (SBP) and Social Security. Review the handout below for an overview of the SBP. Please click on the image to view the PDF.

- Review beneficiary designations on all policies. If you recently got married or divorced, confirm that your beneficiary designations are in line with your current wishes. If you want to name minor children as beneficiaries, it may be a bit more complicated so consider visiting your installation's legal office for assistance.

- Auto, Home, and/or Renters Insurance — Review your policies and let insurers know your spouse is preparing for deployment. Your auto insurance premium may go down because your spouse will not be driving. However, be cautious when cancelling any coverage for your auto or home because premiums may increase when you reinstate the policy.

Make sure you have a will and a power of attorney in place before a deployment.

- Will — A will outlines the distribution of assets at death. Some assets (like life insurance proceeds) pass by beneficiary designation, but not all. It may also appoint a guardian for your children. Review your documents and update any provisions if necessary.

- Power of Attorney — This legal document appoints someone else to make decisions on your behalf. There are general and specific powers of attorney. Your installation’s legal office can advise you on the right path for your situation.

- It is important that both spouses — not just the one deploying — have wills and powers of attorney. Next, make sure you have health care directives, living wills (directives to physicians), medical powers of attorney (health care proxies), and letters of instruction.

- Visit Plan Your Estate for more information on these key estate planning documents.

Here’s Krista who breaks down the importance of family readiness and estate planning.

2

Financial Planning Considerations

Deployments are challenging for families, but they also offer unique opportunities that can help a family improve their financial situation. Take advantage of these special provisions when planning for deployment.

A Service member’s pay during deployment to a qualified combat zone may be excluded from federal taxes (except Medicare and Social Security). This provision means big savings and more money in your pocket. Put these extra resources to work to achieve your financial goals. Review this handout for more information on the Combat Zone Tax Exclusion.

But keep in mind, just because a qualified deployment is tax free, doesn’t mean you don’t have to file your taxes during a deployment. Do your homework!

- Know how deployment will impact your tax situation.

- Make sure you know how to access tax documents.

- Work with an accountant or tax center if needed.

Learn more about how to best prepare by visiting Military OneSource.

Think about your most recent savings account statement. You are probably earning next to nothing in interest. The Savings Deposit Program (SDP) was established by the DoD to provide the opportunity to build savings while deployed to an SDP-eligible combat zone.

The account earns a 10% annual return (compounded monthly, paid quarterly), on up to $10,000. Interest continues to accrue 90 days post-deployment. It is important to note that there are limitations on withdrawing funds in the SDP, so use your budget to determine how much you can afford to put away while still meeting your other goals.

Your Service member needs to set this up after a minimum of 30 days into a deployment. They will have resources available on the deployment. It is important to note the account can’t be closed until redeployment and any emergency withdrawals need approval from a commanding officer. So again, budget wisely for this great savings opportunity.

Click here to visit the Defense Finance and Accounting Service for more information.

Deployments can be a good time to consider increasing your retirement contributions. If you want to make any changes, the service member will have to log into their myPay account here: https://mypay.dfas.mil/#/. Your spouse and their services’s contributions (if covered under BRS) are tax exempt up to the annual limit during a deployment to a designated combat zone. Click here for more information about the TSP contribution limits.

The MLA provides protection from predatory lending and sets limits on interest rates. The SCRA gives Service members the opportunity to cancel contracts (an auto or residential lease, or a cell phone contract, for example) without penalty. The SCRA sets a 6% cap on debt incurred before the Service member joined or was activated. It applies only while on active status. Check to see if these provisions can help save you money during a deployment.

Visit these links to learn more:

Identity theft is an issue we all need to be aware of and take steps to protect ourselves and our families. Here are steps you can take:

- Active Duty Alert — Call one of the three national consumer credit reporting agencies to put an alert in place. This will require additional steps to verify identity if credit is applied for in the Service member’s name. The alert is only good for one year. You may need to call again depending on the length of the deployment.

- Security/Credit Freeze — This step will restrict access to your credit report, which will prevent creditors from approving a new account. You must call all three credit reporting agencies.

Monitor your credit. Make sure you review your credit report and accounts regularly.

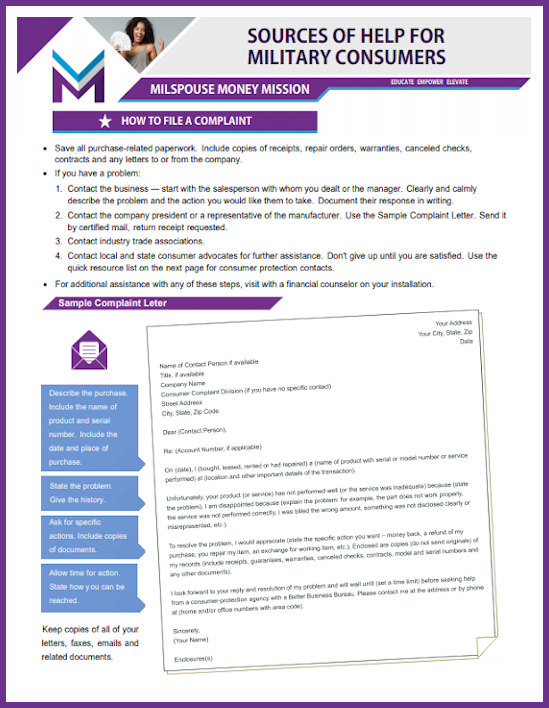

Be mindful and alert to misleading consumer practices! You should report scams to the Federal Trade Commission (FTC) immediately if you find yourself a victim or identify criminal activity. Click here to begin.

Check out Money Ready 201, Protect Your Identity to learn more.

Or review this handout for additional resources for military consumers.

The interest on your spouse's student loans may be suspended for the duration of deployment to a combat zone. Service in a hostile fire area may even qualify for cancellation of some portion of the loan. Remember, the SCRA limits the interest rate to 6% during deployment. Also, make sure to let the loan provider know when the deployment ends.

3

Guard & Reserves

Activated National Guard members and Reservists may qualify for an income-based payment reduction if their income has gone down as a result of the activation.

Health Insurance

You and your family may qualify for TRICARE health coverage if your spouse is an activated member of the National Guard or Reserve. You don’t have to switch, but it is worth investigating to see if you could save some money. Click here for more information.

Credit Relief Act

The SCRA (Servicemembers' Credit Relief Act) can be especially meaningful to members of the National Guard or Reserves because it sets a 6% cap on debt incurred before the Service member joined or was activated. It applies only while on an active duty status.

4

Resources

Please visit the links below for each section to get more information. Deployment is a challenging time, but with knowledge and planning, you can achieve your financial goals and succeed!

Money Ready 201 — Protect Your Identity

Credit Agency Information

- TransUnion — 1-800-916-8800

- Experian — 1-888-397-3742

- Equifax — 1-888-548-7878

Recent Blogs

Giving Military Kids the Tools to Be Financially Capable

Military families are known for resilience, yet the frequent moves, deployments, and changes in income that come with military life can make financial stability feel like a juggling act. But these unique challenges may offer a golden teaching opportunity for military kids. By talking about finances openly and equipping kids with financial skills early on,…

Read More

March Money Moves: Navigating Tax Season While Preparing for Summer Fun

As we welcome the arrival of spring and the promise of warmer weather, it’s easy to get caught up in thoughts of summer plans and family vacations. But with tax season in full swing, it’s important to balance excitement for the upcoming months with a push to wrap up tax season. While those topics couldn’t…

Read More

Communicating with Your Partner About Finances: A February Focus on Financial Wellness

Talking Money with Your Partner As we celebrate loving relationships this month, it’s important to remember that not all conversations come up roses between couples. Sometimes discussing finances can be tricky and stir up negative emotions. Open communication about money is vital for building trust and nurturing a healthy relationship. Whether you’re a new couple…

Read More

Build Financial Wellness from the Ground Up in 2025

There’s something magical about the ball dropping at midnight and turning the page to a new year. For an instant, it feels like you’ve got a clean slate, and anything is possible. In some ways that’s true, but as the calendar page turns, your responsibilities, bills and financial challenges remain. Many people make resolutions to…

Read More

5 Financial Resolutions to Start the New Year Off Right

You don’t need to wait until January to take a fresh look at your finances. Get a jump on the new year with these five resolutions — they can really pay off over the next 12 months. 1. Set/update your budget Setting a budget is the first step in a military family’s financial planning. And…

Read More

5 Financial Power Moves for MilSpouses

During National Veterans and Military Families Month in November, we salute the strength of our families as they support the mission of our community. MilSpouses, especially, display determination as they face the challenges of military life. We see you navigate frequent moves, deployments and often raising children as a solo parent. We understand your motivation…

Read More

The Year In Review: Bring Your Financial Picture into Focus

It can be fun and even eye-opening to watch those year-end montages reminiscing about the year. If you ever have that moment when you say to yourself, “Wait, that was this year?”, you could also imagine how easy it could be to lose track of the goals and financial plans you set in motion when…

Read More

Now’s the Time to Think About Life Insurance

Hey, MilSpouses, it’s Life Insurance Awareness Month! Okay, so maybe that doesn’t make you want to break out the cake and ice cream, but life insurance is an important part of your financial plan. It can help take care of your family, giving them financial security if something happens to you or your service member.…

Read More